3 Retirement Myths Retirees Should Know

3 Retirement Myths Retirees Should Know Get ready to loosen up those purse strings, because we’re about to…

June 21, 2023

Maybe You Shouldn’t Hang Out with Eddie

In this adaptation from Golden Reserve Founder Greg Aler’s new book, Fire Your Financial Advisor, we examine the villainous role Edward Jones has played in creating a retail financial advisor industry that pushes the limits of greed.

When you were in school, your parents probably told you not to hang out with certain kids who weren’t always sticking to the straight and narrow. While you’re now older and wiser, we need to impart one more piece of wisdom. Please, don’t get caught up with that Edward Jones.

Fun fact: both Edward Jones (yes, that Edward Jones) and Golden Reserve founder Greg Aler attended the same small-town Ohio high school, Bellefontaine High. While both would go on to create financial services firms, that’s where the commonalities end. One would build their firm on the founding principle of protecting retirees from high fees and risky investments. The other would build their firm doing…well…the opposite.

In fact, Edward Jones has done much to shape the retail financial advisor industry, but perhaps not in the way you think. So, how was his firm able to grow from nearly $5 billion in revenue in 2013 to more than $12.3 billion in revenue in 2021? A closer look at its overpriced mutual funds, recent settlements and legal proceedings may provide the answers.

Eddie’s Funny Business with Fees

Edward Jones sets the standard (in all the wrong ways) for selling mutual funds with up-front load fees, charging 5% or more. This can be in addition to their ongoing advisory fees –every year at around 1.35%. They may even charge an “exit fee,” should you decide to transfer an account away from Edward Jones.

These fees are astronomical. So why aren’t more people talking about them? Simply put, because they don’t know. Edward Jones discloses the fees in the deepest, darkest corners of their fine print, where you’re least likely to find them.

Eddie’s Kick-Back Scheme

Then there are the allegations of revenue sharing payments– essentially undisclosed kickbacks from mutual fund families Edward Jones recommended to its customers– which landed Eddie in hot water with the SEC. That led to a $75 million settlement in 2004, which may sound like a lot, but really amounted to a drop in the bucket for Edward Jones. Then in 2006, they settled 9 class action lawsuits related to the undisclosed kickbacks with a $127 million settlement. And hey, now they’re disclosing their revenue sharing! You can find it conveniently located in another dark corner of their fine print.

Eddie Won’t Change His Tune

But that’s not where the story ends. In 2018, the company was sued in another lawsuit alleging brokers were pressured to move middle income clients into advisory accounts that could charge up to 2% of assets under management annually, even though the clients engaged in little trading. Eddie did provide disclosures on this one, though the investors in the complaint argue they didn’t receive “full information.” (Perhaps it was located in a different dark corner?)

The closely watched lawsuit has since been dismissed, reintroduced, and in 2022 dismissed again. Regardless of the outcome, the takeaway remains the same: retirees shouldn’t have to worry their savings will be bled to death by high fee investments, or fear what could be hiding in the depths of fine print.

There will always be bad apples; the ones who keep pushing the limits to see what they can get away with. Unfortunately, we believe Edward Jones is one of them. Will the company ever change its tune? It’s doubtful. Which is why in order to stay on the right path in retirement, we tell our friends and family to stay away from Eddie.

———————

Fire Your Financial Advisor is available now on Amazon.com and on our website. To get your copy, or download a free chapter, click here.

_Page_01")

Share this article

3 Retirement Myths Retirees Should Know Get ready to loosen up those purse strings, because we’re about to…

Recently we wrote about the 8x Rule and why it’s a flawed calculation. Yet for many years, it has been…

When it comes to simplifying complex topics, everyone loves an easy to remember rule of…

No matter how good a financial advisor claims to be, no one can predict the…

There are some things in life where you’ll be fine to “wing it.” Unfortunately, paying for long-term…

Chances are you’ve already made assumptions about what your retirement will look like—whether it’s how often you plan to golf,…

Not sure where to put your retirement savings? There’s certainly no shortage of financial professionals’ hawking ideas; but whether…

By now you’ve probably heard plenty about the One Big Beautiful Bill; in fact, you…

You made it to retirement and if ever there were cause for celebration, this is…

For years you’ve dreamed about how you’ll spend your retirement, and now it’s finally here….

Feeling that nagging doubt about your retirement savings? You’re not alone. A recent study found…

“When should you start taking Social Security?” ranks among the top questions researched by retirees….

Retirement is a time to relax and enjoy the fruits of your labor. But how…

Ever wondered how much your financial advisor is really pocketing from your retirement nest egg?…

Retirement should be a time of relaxation and enjoyment, not financial stress or regret. Unfortunately,…

Retirement is a significant milestone, a time to reap the rewards of years of hard…

All our working lives, we dream of what we’ll do with the money we’ve saved…

Recently, a publication targeted toward financial advisors published an article wondering if advisor fees based…

As it turns out, “What Have You Done for Me Lately?” isn’t just a great…

“Set it and forget it,” is the financial industry’s refrain for retirement success; as in,…

Maybe You Shouldn’t Hang Out with Eddie In this adaptation from Golden Reserve Founder Greg…

“Making investment decisions is simple!” said no one ever. But what if there was a…

Downsizing is one of those ubiquitous practices that goes hand-in-hand with retirement, as if moving…

How much should you watch or act on information and predictions that you see on…

Every once in a while, you hear someone say something so succinct and spot-on, you’re…

In this episode: What is different from the big box firms and Golden Reserve with…

The new law raises the Required Minimum Distribution (RMD) age in two steps. The RMD age…

In this adaptation from Golden Reserve Founder Greg Aler’s new book, Fire Your Financial Advisor,…

Podcast: It seems like the Government has your back if your bank fails. Who has…

Golden Reserve Founder Greg Aler pulls back the curtain on how the trillion-dollar financial services…

Even if you love rollercoasters, chances are the rip-roaring stock market isn’t your kind of…

You don’t often hear the word trillion thrown around, unless we’re talking about the U.S….

Let’s talk about the alphabet soup that is the financial services industry. Between the CFPs,…

Poll your friends and family about annuities and you’re bound to get a lot of…

Let’s talk about commissions. For many professions—like real estate agents, sales professionals, brokers and artists—it’s…

Call it the new kid on the block. Fixed index annuities (FIA) are a more…

We recently heard a large, national firm use the slogan, “We do better when you…

We’ve written extensively about the risk of long-term care, but most people don’t want to…

No one likes extra fees, especially when they are hard to understand or being intentionally…

You probably don’t often think about how much your portfolio could go up or down…

Let’s start with a hard truth: you don’t actually own all the money in your…

What is an estate plan? How often should it be updated? What are the essentials…

The IRS may be switching up the regulations for inherited IRAs once again. If it…

We don’t have to explain why the yogurt in the back of your fridge expired….

Like many retirees or soon-to-be retirees, you’re probably hoping to pass on a little financial…

Before you go on a journey, you probably check to make sure you have…

When you open your IRA statement, it’s hard not to feel excited when you see…

If a friend or family member were to ask what your investment style is, would…

It All Comes Down to Want vs. Need Congratulations, you’re the next contestant on The…

Figuring out how and when to elect Social Security can be downright puzzling, especially when it comes to ensuring…

Signs Point to a Change Coming in Q4 Are you biting your nails over…

A report from the not-for-profit Insured Retirement Institute found 50% of boomers—including those who currently…

Ah, annuities: the product the financial services industry loves to hate. But are the hard…

Planning for retirement vs. planning in retirement. What’s the difference, you ask? If the question has you picturing Fred Astaire and Ginger Rogers crooning “to-may-to,…

Find Out What Each Type of Trust Does (or Doesn’t Do) For many of our…

Necessity is the Mother of Invention We’re often asked what the difference is between a retirement planner…

Secret #1: Financial Planners rarely, if ever, consistently beat index returns after netting out their…

Find Out What Makes Us Different from a Financial Advisor For most people, the financial…

Join Forces With Golden Reserve in This Year’s Walk to End Alzheimer’s® Alzheimer’s is anything but an…

If you read our article on the One Thing Your Retirement Plan is Probably Missing,…

Taking Action at These Junctures Can Pay Off When It Matters Most The word “taxes”…

You Could Go It Alone, But Here’s Why We Don’t Recommend It You might have…

Why Now May Be the Time to Act Thinking about retiring? If you have a…

The Two Taxes You’ve Never Heard of but Ought to Know About You’ve worked hard, paid your taxes, and—with the…

The Price Could Be Greater Than You Think Imagine you’re in the lightning round…

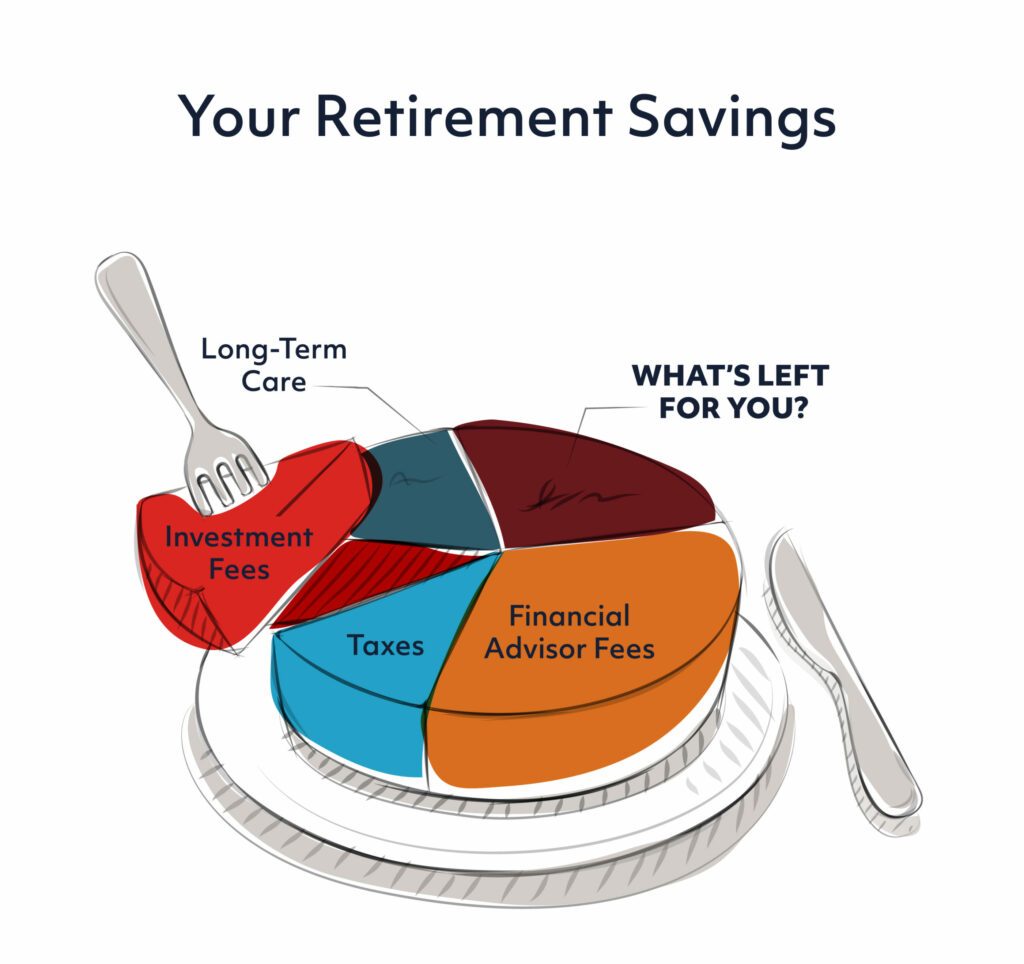

Don’t Let Them Have YOUR Cake and Eat It Too! Preparing for retirement is…

These changes to the capital gains tax would affect nearly everyone. Buckle up, retirees….

Know the difference between fixed and percentage fees Is it rude to ask someone how they make their money?…

No one wants to worry about running out of money. So why are so many plans missing this? Here’s a bit of trivia for you: What’s one of the…

Three Ways to Keep More of Your Hard-Earned Money The only thing that feels…

Let’s Talk About What Keeps You Up at Night If you’re losing sleep over…

Hope is Not Enough When it Comes to Long-Term Care It’s not fun to…

The long-awaited details of US President Donald Trump’s tax plan are finally beginning to emerge….

Just because retirees worry about their health care costs doesn’t mean they’re inclined to comparison…